A Producer's Guide to Financing an Independent Film with Private Equity

The #1 Film Financing Article

Hello, welcome to Scene 7. I’m Lee Rudnicki.

Welcome to the 2025 expanded and improved edition of what might be the most widely read article on film financing in the world. Over the years, this guide has helped more than 10,000 filmmakers, producers, and attorneys understand the ever-evolving world of equity film finance. Many of them have read this article multiple times.

If you're here to learn, you're in the right place.

I’m Lee Rudnicki—an entertainment and technology attorney with over 25 years of experience. I’ve produced independent films around the globe, and I teach this topic in law school. What you’re about to read is practical, tested, and designed to help you navigate the real-world challenges of financing an independent film.

Three quick links.

With this debut, I'm also excited to introduce Scene 7, my new blog exploring the intersection of film, business, and creativity. You can subscribe here:

If you need legal counsel and are interested in learning about my law practice, please visit http://www.LeeRudnicki.com

And finally, I teach a master class for producers, students, and lawyers. For more info, visit: http://www.LeeRudnickiMasterClass.com

Two important notes before we begin the legal discussion:

Plain English, On Purpose.

This article is long because there’s a lot to cover. But it’s written in clear, straightforward language. My mission is to get you to understand the basics of equity film finance. Not to impress you by spouting legal jargon and nonsense that you will not remember or understand.

Not Official Legal Advice.

This is a general overview of a complex topic involving securities laws. While it’s written to make concepts easier to understand, it is not legal advice.

Film financing is not one-size-fits-all. The strategies, structures, and documents that work for one film could be completely wrong—or even illegal—for another. A misstep isn’t just expensive; it can expose you to civil lawsuits, regulatory investigations, or even criminal penalties. If you're serious about raising money, get a qualified attorney.

Bonus - I’ve added some pics to enhance the reader’s experience this time and, more importantly, to break the sections apart and make them easier to digest. If you find these photos to be highly unusual for a professional article drafted by an experienced entertainment attorney … good. :)

Now, let’s dive in to the money on the table!

Part 1 - Private Equity.

For many new producers, the first conversation about financing crashes to a halt the first time someone brings up the term “private equity.”

Yes, it sounds like a technical term from a hedge fund pitch or a corporate meeting. And for those unfamiliar with the business side of film, it can be intimidating. But know this — private equity simply refers to someone investing their own money into your project. That’s it.

Legally speaking, a private equity investor is an individual—or a company, trust, or entity—who provides capital to help fund your offering. And they’re not donating. They’re investing.

As an entertainment attorney, I’ve guided many film clients through this process—successfully raising anywhere from $15,000 to over $30 million. And I can tell you with 100% certainty: when someone other than someone’s mom invests into a film, they expect a return. They want their money back and a premium, usually a screen credit of one form or another, and a percentage of profits, forever.

And potentially, perks like set visitation rights during the shoot.

Part 2 - How “not” to raise money.

One of the most common—and most dangerous—mistakes new producers make is this: they get excited about their project, print out the script, collect a few attachment letters, and start asking people for money.

And sometimes, people say yes. It feels like progress. The dream is taking shape.

But here’s the problem: If you're accepting money for a film without the proper legal structure in place, you are likely violating securities laws.

Film financing is exciting—but it’s a regulated activity governed by state and federal securities laws that protect investors. Ignoring the rules isn’t just risky—it can result in serious consequences, including civil penalties (fines, lawsuits, personal liability, and even criminal penalties (jail).

This is not a gray area. Just because independent filmmaking often feels informal doesn’t mean you can operate as a renegade outside the law. Raising money "under the radar" or through handshake deals may seem efficient—but it's a path to legal trouble. For your project, your investors, and your career.

Beware of Finder’s Fees

In many jurisdictions, paying a finder’s fee to someone who helps you raise money is illegal—especially if that person is not a licensed broker or registered representative. This is because raising capital is a regulated activity under securities laws. When someone introduces you to an investor in exchange for a percentage of the money raised, they are engaging in securities brokerage activity. And unless they are properly licensed, it’s is illegal, full stop.

Violating the rules can have consequences: The offering could be deemed invalid. You may be forced to return investor funds. You could face fines, sanctions, or worse. All of which will ruin your day, and your movie.

Bottom line: Don’t offer anybody a finder fee unless your finder is properly licensed and you are 700% certain of this fact.

Legal counsel is gold.

There are many legal and effective ways to raise money for an independent film. All of them require compliance with applicable securities regulations. Unless you’re launching on Kickstarter or another platform that is legally dialed into compliance by their legal team already, it’s essential to work with a qualified attorney before you accept a single dollar to make a movie.

Part 3 - The PPM

A Private Placement Memorandum (PPM) is a formal legal document that presents your film as an investment opportunity.

Think of a PPM as the bridge between your vision and the financial world. It gives investors the information they need to decide whether to invest in your film.

A PPM typically includes seven key elements, among others: (1) a description of the project, including bios, a synopsis or script, and comparables; (2) a clear explanation of the investment deal terms; (3) financial projections of some kind; (4) use of funds and a preliminary production budget; (5 risk disclosures, required by law; (6) legal disclaimers, also required by law; and (7) a breakdown of how profits will be distributed—commonly referred to as the “waterfall.”

A PPM is NOT a pitch deck or a business plan. It is a legal document, carefully drafted to comply with securities laws and to define the terms of your offering.

As an entertainment attorney, I’ve worked with many clients to develop custom PPMs tailored to their specific projects. Producers cannot—or should not—do this themselves, and there is no universal template online or in print that meets all legal and practical requirements (I’ve done the research).

A proper PPM must reflect your film’s unique budget, structure, goals, and production realities. They range from 80 to 120 pages, depending on the complexity of the offering, and they require significant legal work, including in-depth interviews between the attorney and the producing team. When done right, a PPM accomplishes two critical things: it closes deals—and it protects you legally. And the document protects everyone—both you and your investors.

If drafted correctly, it should not be scary to read for potential investors, it should be interesting, if not exciting.

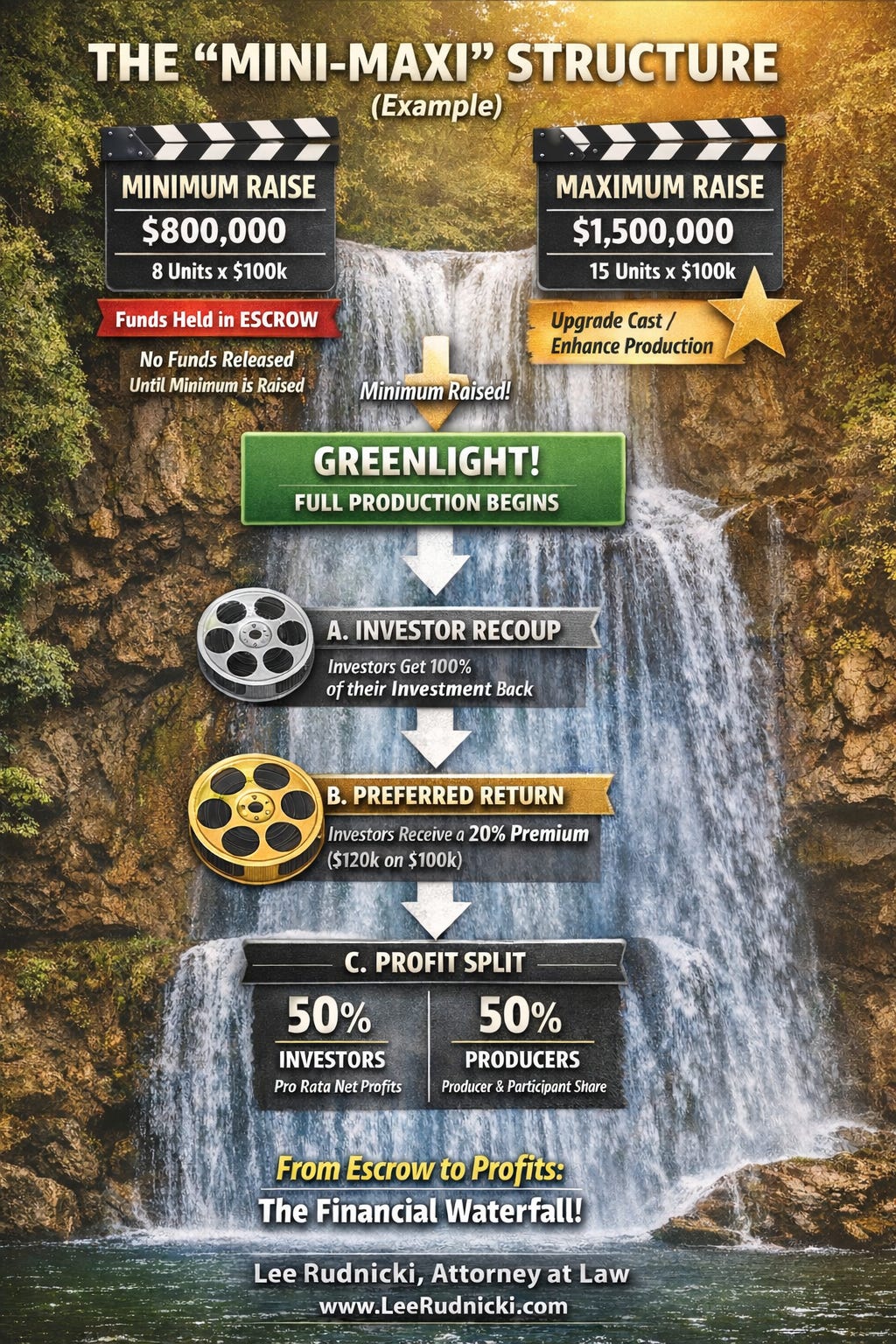

The “Mini-Maxi” Structure

One of the most practical and widely used strategies when structuring a PPM is the “mini-maxi” model. This approach sets both a minimum and maximum fundraising target for your offering.

Your minimum investment represents the lowest amount of capital required to fully produce, complete, and deliver the film—based on hard numbers, not estimates.

Your maximum investment sets a cap or ceiling on the amount you can raise, enabling you to do things like upgrade the cast etc, providing flexibility while also protecting early investors from dilution if the project grows later. For example, if a studio or co-financier joins after the initial round, a defined maximum ensures that original investors retain their proportional share.

Consider a scenario where the minimum budget is $800,000 and the maximum is $1.5 million, with investment units priced at $100,000 each.Until the full $800,000 is raised, investor funds are held in escrow. None of that money is spent on anything (zero).

Escrow is a neutral third-party account where investor funds are held until your minimum raise is met. You can’t access the money early—and that’s the point. Escrow protects investors, demonstrates professionalism, and avoids difficult situations if the financing falls short. No funds are released unless the film is fully financed and ready to roll. That’s the promise you’re making, and escrow is how you keep it.

Once the minimum investment (i.e., your budget) is raised, all funds are released and production is greenlit. Genius!

If the minimum investment is not raised by the time limit specified in your PPM (i.e., nine months), you return ALL of the money to your investors (every penny). Not Genius! BUT – You’re not getting sued!

This provides two key safeguards: first, it prevents you from starting a project you can’t afford to complete, which would be professional doom and years of agony and strained relationships; second, it assures investors their money will not be spent on nonsense before the film is greenlit — which is the reason they felt secure giving you money in the first place.

Part 4 - Deferments

So—you’ve raised the money legally and your production is underway.

What happens when the film begins generating revenue from sales, licensing, streaming, or theatrical release? That’s where the waterfall comes in.

In the film industry, the waterfall refers to the structured order in which incoming revenue is distributed. It determines how investors are repaid, how producers and other participants are compensated, and how profits are ultimately shared. In short, the waterfall defines who gets paid, how much, and when—based on the financial terms you’ve outlined from the start.

Deferments (Bad Idea)

Before going through the waterfall, I want to chat about one concept, the so-called Hollywood “deferment.” Some producers give deferments out like candy, which is bad news all around IMO.

A deferment refers to delaying payment to an actor, crew, or other participants until the film begins making money. So, if you have an actor who gets $1 million a picture, but you can only afford to pay them $500,000 now — you pay the 500k fee and grant them a $500k deferment. At first glance, this may seem like a practical solution. On paper, it allows you to secure talent at a reduced immediate cost.

However, deferments complicate your waterfall and significantly dilute net profits. By deferring payments to multiple parties—actors, writers, producers, or crew—you create a long list of individuals who expect to be paid from early revenue, which disrupts the flow of funds and undermines your ability to offer investors a clear and compelling return.

This deferment is paid in one of two ways, and neither one is good.

OPTION A - The deferment is paid from the first money the producers receive from the film’s distribution. Nightmare scenario = actor gets paid, investors see no money. This is bad for everyone.

OPTION B - The deferment is paid from the first money the producers receive from the film’s distribution AFTER the investors recoup and receive a preferred return. This option is bad for everyone who is entitled to net profirs from the project, including investors.

Worse still, many producers fail to document or manage deferments properly. When the film eventually earns revenue, the lack of transparency can lead to disputes, delays, and in some cases, litigation. As an attorney, I’ve seen the consequences firsthand.

The better approach is to avoid deferments entirely.

As a producer, I never use deferments, full stop. If you cannot afford someone, don’t hire them. Build your budget based on actual resources. This results in a cleaner financial structure, a more reliable waterfall, and a professional presentation to investors—free from hidden obligations and avoidable risks.

Part 5 - The Financial Waterfall

Leaving deferments aside, let’s break the typical independent film waterfall down in simple ABC steps.

A. Investor Recoup

The first priority is straightforward: repay your investors.

B. Investors Preferred Return

After they recoup, the investors get paid a premium agreed upon in your PPM. This premium—often called a "preferred return" compensates investors for the risk they assumed by financing your film.

For example, if an investor contributes $100,000 and the premium is 20%, that investor is entitled to receive a total of $120,000 by the end of this phase.

TIP - Premiums range from 10% to 30%, depending on the raise, the film, and the risk profile.

C. The Profit Split

Next, your film officially moves into profit. From this point forward, any remaining revenue is divided according to the net profit terms outlined in your PPM. A common and widely accepted structure is a 50/50 net profit split: half of the net profits go to the investors, divided pro rata based on each contribution, and the other half is allocated to the producers.

TIP - The producer’s share includes producer profit, creative participant “points,” and other contractual back-end entitlements. For example, if an actor is granted “5% of net profits,” that percentage typically comes from the producer’s half—not the investor’s.

Here is a chart I created to explain the waterfall.

Concepts to understand about Profits

A. All Points Come From the Producer’s Share

Cast, crew, and creative partners profits are taken from the producer’s 50% share. Once investors have been repaid in full, including their premium, their side of the split remains intact. This ensures that investor returns are not diluted by additional creative participants on the back end.

As a result, producers have an incentive to be selective when allocating net profits. Every percentage granted reduces the producer’s share.

B. Net Profits Create Long-Term Engagement

Granting net profit participation, even in small amounts, can foster loyalty and involvement. When someone has a financial stake in a film, they’re likely to remain emotionally and professionally invested beyond production. Whether it’s a lead actor, a key crew member, or a creative collaborator, offering points gives them a reason to promote, support, and champion the film through distribution, release, and beyond.

However, it’s essential that these arrangements are clearly defined and properly documented. Everyone receiving points should fully understand their participation, how net profits are calculated, and when payments may be expected. Transparent, written agreements not only protect your project legally—they also help preserve relationships and prevent misunderstandings.

C. Net Profits Mean Nothing Without a Contract

This is the most important concept in this section.

There is no standard definition of “net profits” in the film industry.

The term “net profits” in your deal may mean something entirely different in someone else’s contract. In some deals, the definition is a single sentence; in others, it spans pages. Studios, independent producers, and financiers each use their own language, formulas, and logic. Sometimes, that language, formulas, and logic is evil, and intended to ensure you never make money.

It’s not unusual for different participants on the same studio film to have entirely different profit definitions. That’s why no one should ever accept an offer like “5% of net profits” at face value. Without a clear, enforceable contract, that promise could be worth a great deal—or absolutely nothing. You have no idea until you read the contract, full stop.

As an attorney, I’ve seen both ends of the spectrum. A well-drafted agreement might assign just 0.01% of net profits and result in substantial earnings. A poorly drafted contract might promise 25% of “gross” profits and ensure you never see a single dollar. In the film business, the contract defines the reality. If you ignore that truth, you do so at your own risk.

Simply put…

Your “Net Profits” only mean what YOUR contract says they mean.

Part 6 - Quick Waterfall Recap

Leaving out deferments (do not use) and bank loans that may require pay back before anyone…

✅ Step One: Investors Recoup their Investment

From the very first dollar that comes in, your investors are first in line.

✅ Step Two: Investor Premium

A pre-agreed premium of 10–30%

✅ Step Three: The Profit Split

50% of the profits go to your investors, split in proportion to their investment.

50% go to the producers, who can then share their portion with cast, crew, and creative partners based on individual deals.

🚫 No Deferments = No Drama, No Chaos

Part 7 - Frequently Asked Questions (FAQ)

Q1: Can I raise money from family and friends without a PPM?

Maybe. It depends on the amount of money, the number of people involved, what state they live in, and how you approach the offer.

Even with friends and family, you can violate securities laws if you’re not careful. The safest move—especially if you're raising more than a few thousand dollars—is to have a proper legal structure and documentation. If you’re unsure, call a lawyer before you call Uncle Bob.

Q2: What’s the difference between an Executive Producer credit and being an equity investor?

An equity investor puts money into the film and expects a financial return.

An Executive Producer credit can be granted for many reasons—money, connections, prestige—but it doesn’t automatically come with a legal right to profits. You can be an Executive Producer and not invest a dime into the movie.

Q3: How do I decide what premium to offer my investors?

There’s no rule, but the range is 10% to 30% over their initial investment. Your premium needs to strike a balance between being attractive to investors and sustainable for your film’. Offering too little won’t get their attention—offering too much might wreck your budget model.

Q4: Can I use a template PPM I found online?

Yikes. Yes, just like you can run through a minefield.

TIP - Read the PPM you found online and make notes of anything you learned, but don’t use it. Random templates are very dangerous in this area of the law. Every film is unique, and securities law compliance is not a copy-paste situation. A bad PPM can get you sued, fined, or worse. If you're serious about raising money, get a custom one drafted by someone who knows what they're doing.

Q5: What if I only raise part of the money I need? Can I still start production?

Not if you're using a proper PPM and escrow structure. The rule is: don’t touch the money until you hit the minimum. This protects the investors—and you—from a half-finished project and a financial disaster. That said, you can raise development funds separately outside the PPM to get your script, package, and materials ready. I have done many of these deals.

This concludes the article.

Thank you for reading, I hope you learned something.

If you’d like to discuss your film or need support with deal structuring, investment documents, or production legal, feel free to reach out—I’m always happy to help. With over 25 years of experience as an entertainment and technology attorney, I’ve represented producers, financiers, and creatives across many independent film and television projects. I know how to protect you and make money at every stage.

Lee Rudnicki, Esq.

http://www.LeeRudnicki.com

Wow this is awesome!! This is a great place to start for any filmmaker.

This is incredibly helpful, Lee. Thanks for being so clear.